The UK cities where you can buy a property with a £10,000 deposit

Following this month’s Budget announcements by the Chancellor regarding the house buying process, many prospective buyers have had a boost of optimism this month.

Not only did the Government confirm the stamp duty holiday extension, but the new mortgage guarantee scheme was unveiled. In response to the long-awaited news of how the government will turn ‘generation rent’ into ‘generation buy’, a selection of lenders will now offer buyers a mortgage, with a 5% deposit, for properties of up to £600,000.

The 15 cities where you can buy a property with a £10,000 deposit

The mortgage experts at money.co.uk have examined the latest house price data, to reveal that there are 15 cities in the UK, where buyers could purchase a home, with a deposit of less than £10,000.

Additionally, the experts analysed the most recent UK salary data to rank the affordability of these cities.

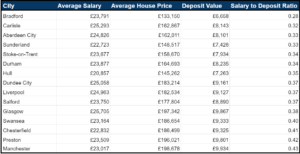

Money.co.uk has additionally discovered that there are 39 cities in the UK where the average value of a deposit is less than £15,000. Of these, the most affordable is Bradford, where the average property price sits at £133,150.

With the help of the government’s new guarantee scheme, the average buyer deposit in the city would total £6,658. This is around a quarter of the average Bradford annual salary.

In contrast, those wanting to secure a property in Bradford with a deposit of 15% would be required to put down £19,973. Outside of Bradford, buyers looking for an 85% LTV mortgage, would need to fork out a deposit of over £20,000 across all UK cities.

Research also found that Carlisle, Aberdeen City and Sunderland are also a solid option for those looking to purchase a property with a low deposit (deposit of £8,143, £8,101 and £7,426 respectively).

London is the least affordable city to buy a property in. However, despite the higher income to deposit ratio, those hoping to purchase a home in London will benefit the most from the 5% deposit scheme.

The average property in London totals £644,631. On average, prospective buyers would have to save up almost £96,695, with an 85% LTV mortgage. Therefore, while the 5% ask of £32,231 is still a pricey sum, it elevates the pressure of saving an additional £64,464.