Construction start performance continues to decline, but negative curves start to soften

Today, Glenigan, the construction industry’s insight expert, releases the March 2022 edition of its Construction Index.

The Index focuses on February 2022, covering all projects with a total value of £100m or less (unless otherwise indicated), with all figures seasonally adjusted.

It’s a report which provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the last 12 months.

Silver Linings

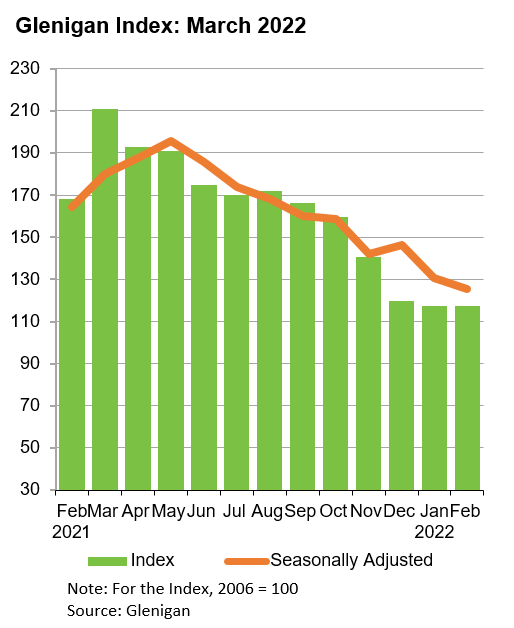

Although decline continued into February, making it the weakest on record, performance-wise since 2015, a strengthening pipeline of planning approvals and main contract awards indicates future, if not immediate, recovery.

This month’s Index shows that, the downward curve, which has persisted since spring 2021, is starting to soften. Supply chain issues might continue to bite, but are less aggressive in material terms.

Glenigan Index March 2022.png

However, socio-economic ructions caused by the Russia-Ukraine situation will no doubt have an effect as fuel and energy prices are likely to rocket in Q.2 and Q.3. However, the full impact is still too early to appreciate.

Sector Analysis – Residential

Private housing experienced one of the worst overall performances of any sector during this period, with the value of project starts declining by 23% against the preceding three months (to February 2022), standing 50% lower than a year ago.

Social housing fared little better, having remained relatively robust in the preceding months, falling 16% during the period and 26% compared with the previous year.

Looking at the sector overall, work commencing on site fell 21% during the three months to February, and were 46% lower than the previous year.

Sector Specific – Non-Residential

It was a mixed bag in the non-residential sector, however, a few trends are starting to emerge which indicate post-COVID resurgence.

Last month, the Index reported that hotel & leisure grew (23% on the preceding year, and 35% in the three months to January). Once more, the sector has increased performance-wise, standing 23% on the preceding the three months to February and 7% higher than a year ago.

Community & amenity was another March index high-riser, experiencing a spike in activity. Starts jumped 28% against the preceding 3 months and 38% compared with a year ago.

Industrial-starts, the consistent star performer in Index terms, declined 17% during the three-month period covered by the Index. However, the vertical remained steadfast, up 19% on the previous year.

Sprinting ahead, office construction-starts increased by nearly a fifth (17%) in the three months to end of February, but fell marginally short compared to 2021 levels (-6%)

Education and health-starts fell, reflecting a steady decline in both sectors, which will no doubt throw the Government’s levelling-up policy open to scrutiny.

Whilst infrastructure construction-starts indicated green shoots of recovery, increasing 2% during the three months to February, the value fell 27% compared to 2021.

Modest increases will be tempered by another sharp fall for civils work, down 17% against the preceding three months and 34% compared with a year ago. The utilities sector added further salt to the wound once again posting big losses in start terms, falling 43% against the preceding three months to February to stand 48% lower than a year ago.

Regional Analysis

The North East was the best performer during the three months to February, and the only one that experienced growth against this period and 2021 (+6%).

Inconsistency reigned supreme in the other regions. Scotland experienced the greatest increase in project starts against the preceding three months (+13%), but was down 36% on a year ago. Similarly, project starts in London declined by over a quarter (26%) compared to 2021, but increased during the three months to February. The South East was the only other region to experience growth against the preceding three months (+4%).

Unfortunately, all other regions returned poor performances. The value of project starts fell in the West Midlands by 41% during the three months to February, standing 54% lower compared to a year ago. Strong declines were also seen in the East Midlands, East of England, North West and South West on both the Index period covered and 2021.

Commenting on the Index’s findings, Glenigan’s Senior Economist, Rhys Gadsby says, “We urge readers of this Index to maintain a positive outlook. Whilst project starts remain low, the downward curve is softening and, as our most recent Forecast predicted, a gradual rise in the latter half of 2022 is likely.

He adds, “External events are skewing the market and no doubt current geopolitical events in Eastern Europe will create some challenges. However, the UK construction industry is incredibly resourceful, and the strong pipeline of planning approvals and contract wins is testament to this. In our view it’s very much a case of ‘keep calm and carry on’.